ECONOMYNEXT – The self-congratulatory and almost gloating terms in which the return of monetary depreciation and accompanying rise in the cost of living towards the central bank’s inflation target is welcomed by macro-economists is in bad taste.

Inflation is nothing other than an immoral philosophy cooked up by post-1960s macroeconomists who rejected classical economic theory for statistics and visited great privations upon vast populations.

The return of depreciation and inflation which will eat into consumption undermining living standards, put capital expenditure projects out kilter by inflating planned costs and sabotage plans by the government to bring down electricity costs, is nothing to crow about.

Though it may give short term profits to companies and banks and early customers that are closest to the inflationary operations of the central bank, inflation and depreciation will kill growth and costs will ultimately catch up.

Gloating over the rising cost of living?

“The current low level of inflation, at 1.6 percent (y-o-y) in February 2026, relative to the target of 5 percent, provides sufficient space to accommodate the impact of higher energy prices and their spillovers on inflation,” the central bank claimed in its last monetary policy statement after depreciating the rupee from 300 to 315 after printing money through swaps and denying convertibility for more than a year.

“Given the latest available data and prevailing uncertainties, inflation is now expected to reach the target of 5 percent in Q2-2026, earlier than previously anticipated,” the central bank statement added in self-congratulatory terms.

“Inflation is projected to remain around the target thereafter. available data and prevailing uncertainties, inflation is now expected to reach the target of 5 percent in Q2-2026, earlier than previously anticipated.

“Inflation is projected to remain around the target thereafter.”

Where is the space in the people’s family finances?

How can the central bank claim there is ‘space’ to accommodate higher prices, after destroying people’s wages, pensions and Employees Provident Fund balances by busting the rupee from 184 to 300 from 2022 to 2023 and from 131 to 184 to the US dollar from 2015.

What family has ‘space to accommodate’ the rise in cost of living?

How can a state agency frame the hardships it inflicts on the poor, with higher food and energy prices, the overall reduction of disposable incomes of the citizenry of a nation, and the losses it inflicts on state enterprises with dollar debt and the expansion of foreign debt, in these almost gloating terms.

Does it not remember that by busting the rupee from 184 to 300 to the dollar, it made the population fall on all fours, destroying wages and pushed a large section of the populace into poverty and marginal income brackets into near starvation and made them skip meals?

How can this state agency rejoice as the meagre salary increments the people got over the past year as the economy limped back to a recovery are further destroyed in 2026?

The International Monetary Fund was no better, framing the hardships of the poor in positive terms.

“The economy grew by 5 percent year on year in 2025,” the IMF said in a statement. “Inflation has returned to positive territory and rebounded to 2.2 percent year on year in March.”

The return of inflation, the destruction of wages of the poor, rising food and energy prices is nothing to celebrate as ‘rebounded’.

Sri Lanka’s economic growth ‘rebounded’ to 5 percent, not due to inflation as macro-economists try to make their victims believe, but due to the lack of inflation and lack of monetary depreciation that made prices predictable and real wages to rise, however slowly.

Recovery from Say’s law not inflation and stimulus

This is not a recovery from inflation or stimulus as touted by macroeconomists, post-2000 inflationist central bankers, out of the closet Keynesians, and the ‘policy support’ often touted by the some IMF officials also, but the Say’s Law in action.

The recovery was also helped by the current leadership of the central bank itself appreciating the currency back to 300 to 360 to the US dollar and preventing further inflation of housing, education and health care and transport costs.

But the effects of that original destruction of the rupee which radically altered the price structure of traded goods and wages, and also the pre 2022 destruction of the, rupee is still working through services like private education, housing costs and rents, while wages of most people lag.

That is why governments were ousted after the rate cuts to reach the 5-percent inflation target triggered currency depreciation without a war in Sri Lanka.

There is no ‘wage spiral inflation’ as macro-economists and post -1960s central bankers so craftily claim.

Workers strike because food and energy prices, which respond fastest to money printing and depreciation, have made their life miserable, but are not captured in some indices due to core-inflation or because they are loaded with services and rents which take time to go up.

Effects of Inflation

Strikes and wage hikes are a result of central bank inflationary policy and are not the cause of price rises.

Price rises are but one of several results of inflationary policy. Over issue of reserve money (above a credible anchor required for sound money) is what classical economists called ‘inflation’ in the first place.

Central-bank-generated-inflation has complex unfortunate effects, where increases in commodity prices, and increases in price indices are but one immediate effect.

In a reserve collecting central bank regime, forex shortages and depreciation are also early effects which are seen about four to six weeks after liquidity is injected, when there is strong credit growth.

Other key results include asset price bubbles and mal-investments, which result in burst bubbles and massive economic crises even in floating rate regimes, where currency crises are not possible.

The central bank’s inflationary swaps with commercial banks have also set off a chain reaction showing the effects of reserve money inflation.

Now finance companies which earlier had no access to the central bank’s inflationary windows are swapping dollars to commercial banks, which in turn are swapping them to the central bank and giving loans. All of which of course ends up in the forex market like the George Soros’ fx swaps in the East Asian crisis.

The central bank itself has given its staff massive salary hikes. Certainly, central bank staff have ‘space’ in their family finances to absorb a 5 percent a year rise in cost of living generated by their employer.

But hardly anyone else. A cursory look at job advertising sites shows how little salaries have increased since the last currency collapse in 2022 from inflationary rate cuts.

People who got 300 to 500 dollar equivalent salaries in 2015 when this flexible inflation targeting potential/output targeting/REER targeting began to hit the country are still not getting the same salaries yet in dollar terms.

The central bank’s salary hikes, and defined benefit pensions, which allow the agency to escape the Cantillon effects it visits upon the nation also dates back to the IMF’s Second Amendment to its articles in the 1980s and represents escaping accountability for its inflationism.

Exchange rate as the first line of defence, now promoted by IMF against its founding principles is also an institutionalized tactic to escape accountability for denying convertibility to liquidity from inflationary rate cuts and in the case of 2025 and 2026 in particular, inflationary fx swaps.

Monetary Depreciation and Coin Clipping

Destroying the value of the monetary unit was a punishable crime before the age of inflation and social unrest triggered by unaccountable state-run central banks.

Before fiat money the destroying the value of the monetary unit was accomplished by more transparent means including coin clipping, which was criminalized.

Depreciation of paper was also not allowed, until the IMF’s Second Amendment to its articles, legitimized the practice, wreaking havoc in developing countries and Latin America.

Though the Washington Consensus of the 1980s involving ‘competitive exchange rates’ also legitimized unsound money, which went against the main objective of creating the IMF in the first place after World War II, the Federal Reserve under Paul Volcker was for sound money.

Volcker said in his memoirs later that he did not study either Keynesianism, or take Economics 101, but went into an advanced economic course and studied money and banking under two Austrian economists.

“Both were taught by distinguished refuge scholars of the classic Austrian liberal school of economics, Oskar Morgentern and Friedrich Lutz,” Volcker recalled in the Quest for Sound Money and Government

“They emphasized the works of free-market advocates, including Ludwig von Mises and Friedrich Hayek from Eastern Europe.

“While it hardly seems possible, to the best of my memory John Maynard Keynes and his theories in the English tradition of advocating active government policies to manage the economy received no attention.”

The US was lucky that Volcker, who did not believe in inflationary policy unlike Sri Lanka’s central bank that gets IMF technical advice for the single policy rate, or flexible policy, was alive to be appointed as Fed Chief, and the economic strategists of the Carter administration believed in sound money.

East Asian nations (and China in the 1990s), which piggy backed on the dollar in the 1980s with deflationary policy, ended up as export and investment powerhouses that exported capital. Amid the ample reserves regime, the Asian savings glut is no more.

Sri Lanka, which piggy backed on the IMF’s Second Amendment and ‘competitive exchange rates’ in the 1980s ended up with discredited economic reforms, social unrest and authoritative governments.

The US and the world were even luckier that the Reagan administration which followed had similar beliefs to the Carter administration that appointed Volcker.

There is no such consensus or even knowledge now with inflationists running central banks with statistics (data driven monetary policy) rather than economic theory and politicians not getting involved in central banks except in Singapore and members ruling families in GCC countries.

As a result, even if governments change, the central bank will continue to generate inflation and depreciate the currency. This was Sri Lanka’s experience after the end of the civil war.

With the rupee at 315 in the spot market and 320 for imports now, which shows the deep flaws in the operating framework of the central bank, Sri Lanka is once again on the post-civil war path.

The recent capital flight from rupee bonds is only one sign of it.

An Immoral Philosophy

It is not just that the Jean-Baptiste Say was proved in Sri Lanka and Keynesianism (IMF’s ‘policy support’ and targeting potential output) defeated comprehensively by the rapid recovery in economic activity, amid so-called deflation so hated by the inflationist central bankers in this age of inflation.

The horrific reflation doctrine that destroyed the US, Europe from around 2000, and also Sri Lanka from around 2012 and intensified into an institutionalized doctrine from 2015, leading to a frenzy of foreign borrowings and eventual default has been debunked repeatedly by classical economists for at least two centuries until World War I.

The effects of Sri Lanka’s last rate cut have been covered up by inflationary swaps indebting a state agency and exposing it to forex risks and depreciation in the process.

Rates cannot be cut by expanding reserve money or ‘circulating medium’ as originally proposed by John Law.

It is a spurious doctrine debunked repeatedly by classical economists for over two centuries and until the Fed started open market operations in the 1920s triggering the Great Depression.

Rates are a function of capital. If capital is destroyed by depreciating the value of the monetary unit, interest rates will not fall.

Steep depreciation and inflation will lead to higher interest rates and destroyed budgets, as they did in Sri Lanka from the IMF’s Second Amendment in the 1980s.

Neither will there be capital to invest or repay debt.

There will be SOE forex losses including in SriLankan. India’s Indigo and Air India is now in similar trouble with the Reserve Bank of India depreciating the rupee.

READ MORE : IndiGo Q2FY26 loss widens to Rs 2,582 crore on forex loss

Qatar Air and Emirates are doing very well on that front, thank you very much, despite real bombs falling on the country, and no macro-economists dropping monetary bombshells to destroy currencies and finances of the airlines.

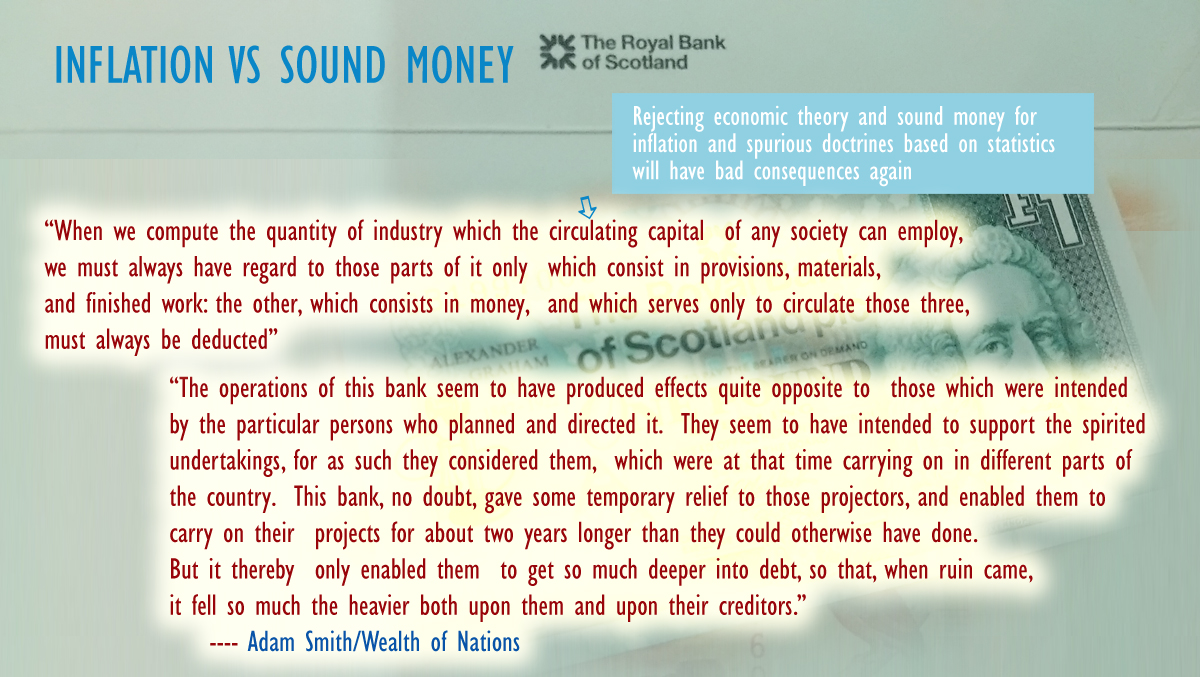

It is not possible to run a country or a business with a note issue bank that rejects economic theory and the carefully reasoned explanations of Hume or Ricardo or Smith as well as the Germans who resisted Keynes.

No person, no central banker, who has read at least the Chapter Two of Book II of the Wealth of Nations (Of Money Considered as a particular Branch of the General Stock of the Society, or of the Expence of Maintaining the National Capital) and understood the import what Adam Smith was explaining will ever try to cut rates by expanding reserve money.

That is why Sri Lanka’s interest rates rise sharply after rate cuts trigger currency crises.

Adam Smith did not study macro-economics or stimulus or central bank ‘policy support’ or potential output targeting, or single policy rates for that matter, which is an extreme form of inflationary policy.

Economics or political economy as the discipline was first known, was not yet in existence and mercantilism was the dominant philosophy. Adam Smith studied moral philosophy.

The belief in inflation by the agency which is supposed to provide a stable monetary unit is an immoral philosophy.

To disclaim responsibility for liquidity injections including through buy-sell swaps and deny convertibility to destroy the value of a currency of a nation claiming it is ‘market determined’ is also immoral.

It is also immoral to impose exchange controls and trade controls on the citizenry after printing money including through swaps and creating forex shortages.

It is even more immoral to threaten to fine and jail the unfortunate public, who are trying to avoid using the depreciating money of an inflationist central bank.

It is duplicitous to give ‘Aswesuma’ under IMF programs after depreciating the currency with swaps, or excessive dollar purchases and denying convertibility to the printed rupees, hitting the poor and those in marginal income brackets the hardest with the inflation target.

The horrific false doctrine of inflation driven growth (some macro-economists claim that money is neutral and non-neutral in the same breath) is based on cheating wage earners with the Cantillon effect.

That is why the electorates rise up against the government. They have no idea that the perpetrator is the inflationist central bank.

The monetary depreciation which has amplified an external shock and internalized it, has been carried out with inflation below 2 percent. Earlier crises were triggered also below 5 percent inflation. For a central bank with exchange rate policy, no inflation target is a sufficient constraint.

Sri Lanka’s parliament has erred, and erred terribly, in giving ‘independence’ to a central bank that believes in 5 percent inflation and monetary depreciation.

That wrong has to be corrected with a true monetary constitution that restrains the inflationary operations of the monopoly note-issue bank, or its monopoly broken, if this country is to progress and democracy is to prevail.

Continue Reading

Leave a Reply